Financial Planning for Business Owners

Our Process

Some of the biggest benefits of owning a business are the tax-savings opportunities available to small business owners (sole-proprietors, partnerships and incorporated businesses).

This starts with being able to claim for business some expenses that you would normally be paying for anyway (such as a reasonable part of your car expenses, your home office, cell phone, etc.). It can also end with you being able to claim up to $406,800 tax-free from the sale of your “Qualified Small Business Corporation”.

You can also use your corporation to save on taxes for your medical & dental expenses (through the Personal Health Savings Plan), your Critical Illness Plan (with extra tax savings when paired with a Return of Premium rider), and your life insurance (that can be passed on with tax-savings through the CDA/Capital Dividend Account).

All it takes is some proactive planning – because the day before you file your tax return is just a little too late to take advantage of these benefits.

On the other hand, the biggest risk to a business is probably the death or illness of key personnel.

So if you or someone in your organization is key to keeping the business going, it’s essential to have solutions in place to help make sure your business can ride through the wave of a sudden serious accident, major illness, or death of that key person.

This can include not only disability, critical illness or life insurance, but also financial plans to support your back-up plans to keep your business operating and avoid losing your customers.

After all, when you’ve worked so hard to get through the beginning years, you really wouldn’t want unexpected circumstances to put your back to where you started – or worse, in major debt.

So call me for a review of your old business financial plan or if you’d like a fresh set of eyes on it. I can also give you information on some not-so-common but can-be-very-effective tax-savings ideas that you can review with your business tax accountant (that he or she may not be quite familiar with).

Articles with Tax Savings & Business Continuity Ideas for your Small Business

https://dytucofinancialservices.com/wp-content/uploads/2020/04/business-chairs-company-coworking-7070.jpg

423

640

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-04-16 13:23:282020-04-16 21:18:15New Canada Emergency Commercial Rent Assistance | Canada Emergency Business Account Expanded

https://dytucofinancialservices.com/wp-content/uploads/2020/04/business-chairs-company-coworking-7070.jpg

423

640

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-04-16 13:23:282020-04-16 21:18:15New Canada Emergency Commercial Rent Assistance | Canada Emergency Business Account Expanded https://dytucofinancialservices.com/wp-content/uploads/2020/04/CERB_expanded.png

320

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-04-15 09:49:412020-04-23 16:00:47Expanded eligibility for Canada Emergency Response Benefit (CERB) & Boosted wages for Essential Workers

https://dytucofinancialservices.com/wp-content/uploads/2020/04/CERB_expanded.png

320

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-04-15 09:49:412020-04-23 16:00:47Expanded eligibility for Canada Emergency Response Benefit (CERB) & Boosted wages for Essential Workers https://dytucofinancialservices.com/wp-content/uploads/2020/04/CEBA_Today.png

320

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-04-09 10:47:222020-04-09 18:39:12Applications for the Canada Emergency Business Account starts TODAY!

https://dytucofinancialservices.com/wp-content/uploads/2020/04/CEBA_Today.png

320

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-04-09 10:47:222020-04-09 18:39:12Applications for the Canada Emergency Business Account starts TODAY! https://dytucofinancialservices.com/wp-content/uploads/2020/04/Business_Owners_Qualification_850px.png

600

850

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

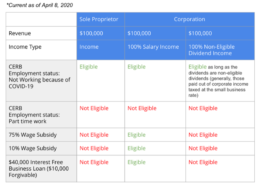

Dytuco Financial2020-04-08 15:50:562020-04-08 23:54:14Rules changed to allow more struggling business owners access to CERB, Wage Subsidy. Summer jobs program increased to 100%

https://dytucofinancialservices.com/wp-content/uploads/2020/04/Business_Owners_Qualification_850px.png

600

850

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-04-08 15:50:562020-04-08 23:54:14Rules changed to allow more struggling business owners access to CERB, Wage Subsidy. Summer jobs program increased to 100% https://dytucofinancialservices.com/wp-content/uploads/2020/03/CERB_and_EI-500x320-2.png

320

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-03-30 10:46:102020-03-31 17:09:15Do I Qualify for the Canada Emergency Response Benefit & EI?

https://dytucofinancialservices.com/wp-content/uploads/2020/03/CERB_and_EI-500x320-2.png

320

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-03-30 10:46:102020-03-31 17:09:15Do I Qualify for the Canada Emergency Response Benefit & EI? https://dytucofinancialservices.com/wp-content/uploads/2020/03/Trudeau-Wage_subsidy_75percent.png

337

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-03-27 11:40:562020-03-27 20:12:23Help for Small/Medium Businesses & Entrepreneurs – 75% wage subsidy, $40,000 interest-free loan & more

https://dytucofinancialservices.com/wp-content/uploads/2020/03/Trudeau-Wage_subsidy_75percent.png

337

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-03-27 11:40:562020-03-27 20:12:23Help for Small/Medium Businesses & Entrepreneurs – 75% wage subsidy, $40,000 interest-free loan & more https://dytucofinancialservices.com/wp-content/uploads/2020/03/SupportForRenters-500px.jpg

281

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-03-26 11:18:172020-03-26 18:57:08BC Government supporting renters, landlords during COVID-19

https://dytucofinancialservices.com/wp-content/uploads/2020/03/SupportForRenters-500px.jpg

281

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-03-26 11:18:172020-03-26 18:57:08BC Government supporting renters, landlords during COVID-19 https://dytucofinancialservices.com/wp-content/uploads/2020/03/Canada_Emergency_Response_Benefit-500px.png

362

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-03-25 13:15:392020-03-25 21:30:11Canada Emergency Response Benefit to help workers and businesses

https://dytucofinancialservices.com/wp-content/uploads/2020/03/Canada_Emergency_Response_Benefit-500px.png

362

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-03-25 13:15:392020-03-25 21:30:11Canada Emergency Response Benefit to help workers and businesses https://dytucofinancialservices.com/wp-content/uploads/2020/02/BC_BUDGET_2020.png

500

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-02-19 16:27:412020-05-05 06:15:332020 BC Budget

https://dytucofinancialservices.com/wp-content/uploads/2020/02/BC_BUDGET_2020.png

500

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-02-19 16:27:412020-05-05 06:15:332020 BC Budget https://dytucofinancialservices.com/wp-content/uploads/2020/01/rrspTFSA.png

512

1024

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-01-23 14:47:022020-01-23 23:00:19Comparing TFSAs and RRSPs – 2020

https://dytucofinancialservices.com/wp-content/uploads/2020/01/rrspTFSA.png

512

1024

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-01-23 14:47:022020-01-23 23:00:19Comparing TFSAs and RRSPs – 2020 https://dytucofinancialservices.com/wp-content/uploads/2020/01/5ReasonsRRSPSquare.jpg

500

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-01-23 14:05:002020-01-25 19:22:45Top 5 Ways to Use an RRSP to Help You Save Taxes

https://dytucofinancialservices.com/wp-content/uploads/2020/01/5ReasonsRRSPSquare.jpg

500

500

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-01-23 14:05:002020-01-25 19:22:45Top 5 Ways to Use an RRSP to Help You Save Taxes https://dytucofinancialservices.com/wp-content/uploads/2020/01/2020CheatSheetFI.png

810

1440

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-01-16 11:23:182020-01-16 19:36:072020 Financial Facts for Business Owners

https://dytucofinancialservices.com/wp-content/uploads/2020/01/2020CheatSheetFI.png

810

1440

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2020-01-16 11:23:182020-01-16 19:36:072020 Financial Facts for Business Owners