https://dytucofinancialservices.com/wp-content/uploads/2016/05/Cascading-copy.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-05-01 08:00:322016-05-26 23:14:39Beyond Tax-Savings: The Benefits of an Estate Bond for your Estate Beneficiaries

https://dytucofinancialservices.com/wp-content/uploads/2016/05/Cascading-copy.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-05-01 08:00:322016-05-26 23:14:39Beyond Tax-Savings: The Benefits of an Estate Bond for your Estate Beneficiaries https://dytucofinancialservices.com/wp-content/uploads/2016/05/Questions-000103-0018-001260.jpg

1701

2400

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-05-01 06:39:502016-05-31 21:13:21Understanding your life insurance options

https://dytucofinancialservices.com/wp-content/uploads/2016/05/Questions-000103-0018-001260.jpg

1701

2400

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

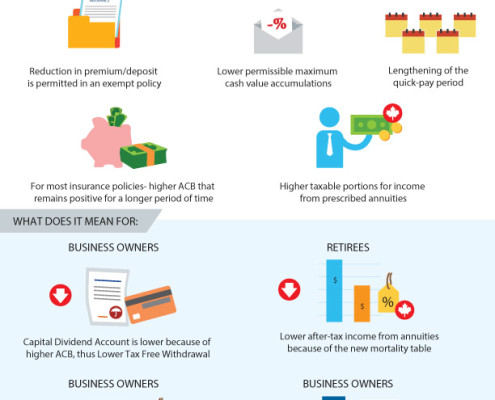

Dytuco Financial2016-05-01 06:39:502016-05-31 21:13:21Understanding your life insurance options https://dytucofinancialservices.com/wp-content/uploads/2016/04/exemptTestLegislation-1.jpg

792

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-04-01 20:41:032016-08-26 15:37:38Tax-Exempt Legislation Changes

https://dytucofinancialservices.com/wp-content/uploads/2016/04/exemptTestLegislation-1.jpg

792

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-04-01 20:41:032016-08-26 15:37:38Tax-Exempt Legislation Changes https://dytucofinancialservices.com/wp-content/uploads/2016/01/Estate-Bond.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-04-01 08:00:572016-11-04 18:08:48A Lifetime Gift for Your Grandchildren

https://dytucofinancialservices.com/wp-content/uploads/2016/01/Estate-Bond.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-04-01 08:00:572016-11-04 18:08:48A Lifetime Gift for Your Grandchildren https://dytucofinancialservices.com/wp-content/uploads/2016/03/budget-1.jpg

688

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

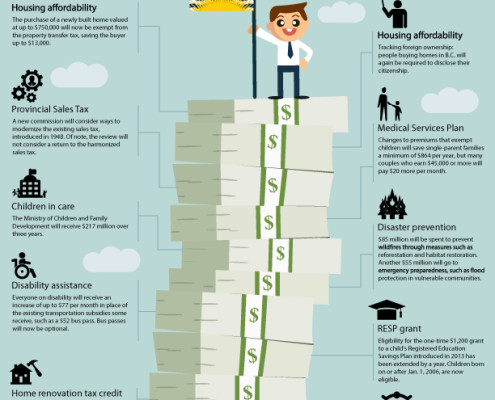

Dytuco Financial2016-03-19 20:25:432016-04-07 21:35:13BC Budget Changes

https://dytucofinancialservices.com/wp-content/uploads/2016/03/budget-1.jpg

688

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-03-19 20:25:432016-04-07 21:35:13BC Budget Changes https://dytucofinancialservices.com/wp-content/uploads/2016/01/iStock_000008480354Small.jpg

565

849

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-03-06 08:00:222016-04-23 15:55:53Estate Planning for Real Estate Investors

https://dytucofinancialservices.com/wp-content/uploads/2016/01/iStock_000008480354Small.jpg

565

849

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-03-06 08:00:222016-04-23 15:55:53Estate Planning for Real Estate Investors https://dytucofinancialservices.com/wp-content/uploads/2016/02/Losing-money-000100-0046-000123.jpg

1703

2400

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-02-22 18:55:322016-04-23 15:53:23Leave a Financial Legacy for your family and less taxes for the government

https://dytucofinancialservices.com/wp-content/uploads/2016/02/Losing-money-000100-0046-000123.jpg

1703

2400

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-02-22 18:55:322016-04-23 15:53:23Leave a Financial Legacy for your family and less taxes for the government https://dytucofinancialservices.com/wp-content/uploads/2016/01/pot-of-gold-78ka_row5_130301-smaller.jpg

750

900

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-01-05 09:27:222016-04-23 15:56:1810 often overlooked places to look for savings

https://dytucofinancialservices.com/wp-content/uploads/2016/01/pot-of-gold-78ka_row5_130301-smaller.jpg

750

900

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-01-05 09:27:222016-04-23 15:56:1810 often overlooked places to look for savings https://dytucofinancialservices.com/wp-content/uploads/2016/01/rrspOrTfsa-01.jpg

792

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-01-03 08:00:532017-02-06 05:40:01TFSA or RRSP?

https://dytucofinancialservices.com/wp-content/uploads/2016/01/rrspOrTfsa-01.jpg

792

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-01-03 08:00:532017-02-06 05:40:01TFSA or RRSP? https://dytucofinancialservices.com/wp-content/uploads/2016/01/iStock_000006962623Small.jpg

565

849

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-01-03 08:00:372016-04-23 15:54:29Taxation Changes for Life Insurance Create Tax-Savings Opportunities in 2016

https://dytucofinancialservices.com/wp-content/uploads/2016/01/iStock_000006962623Small.jpg

565

849

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2026/05/BusinessCard-MMD-front-2026-05-CFP-only.jpg

Dytuco Financial2016-01-03 08:00:372016-04-23 15:54:29Taxation Changes for Life Insurance Create Tax-Savings Opportunities in 2016