Financial Planning at any Age

Video created by Jaime Munro from Whisper Media (www.whispermedia.ca)

Needs vary as we go through different life stages. For example, needs and priorities may include:

Starters (age 21 to 34 – finishing school or starting on career path):

Builders (age 35 to 44 – may have kids and own a home):

Accumulators (age 45 to 54 – may be progressing in their career and/or have grown young adult children):

Accelerators (age 55 to 64 – may be preparing for retirement):

Preservers (age 65+ may be retired and still active):

https://dytucofinancialservices.com/wp-content/uploads/2016/08/iStock_000020364006XSmall-e1449699724537-175x1501.jpg

150

175

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-09-01 05:01:462016-09-27 00:33:03Canada Pension Plan – Should You Take it Early?

https://dytucofinancialservices.com/wp-content/uploads/2016/08/iStock_000020364006XSmall-e1449699724537-175x1501.jpg

150

175

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-09-01 05:01:462016-09-27 00:33:03Canada Pension Plan – Should You Take it Early? https://dytucofinancialservices.com/wp-content/uploads/2016/07/Danger-000568-0115-000024.jpg

533

800

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-07-20 22:45:362016-10-20 04:59:12Creative Risk Management Planning for your Business

https://dytucofinancialservices.com/wp-content/uploads/2016/07/Danger-000568-0115-000024.jpg

533

800

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-07-20 22:45:362016-10-20 04:59:12Creative Risk Management Planning for your Business https://dytucofinancialservices.com/wp-content/uploads/2016/01/Blended-families-1.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-06-01 08:00:182016-07-08 17:35:05Estate Planning for Blended Families

https://dytucofinancialservices.com/wp-content/uploads/2016/01/Blended-families-1.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-06-01 08:00:182016-07-08 17:35:05Estate Planning for Blended Families https://dytucofinancialservices.com/wp-content/uploads/2016/01/beneficiary-designation-1.jpg

196

425

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-06-01 08:00:052016-10-20 05:23:16Pay Attention to Your Beneficiary Designation

https://dytucofinancialservices.com/wp-content/uploads/2016/01/beneficiary-designation-1.jpg

196

425

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-06-01 08:00:052016-10-20 05:23:16Pay Attention to Your Beneficiary Designation https://dytucofinancialservices.com/wp-content/uploads/2016/05/Safe_opening_b2-b7.jpg

2400

1693

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-05-15 05:29:342017-02-06 05:52:08A Tax Savings Solution Using a Corporate Health Plan

https://dytucofinancialservices.com/wp-content/uploads/2016/05/Safe_opening_b2-b7.jpg

2400

1693

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-05-15 05:29:342017-02-06 05:52:08A Tax Savings Solution Using a Corporate Health Plan https://dytucofinancialservices.com/wp-content/uploads/2016/05/Cascading-copy.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-05-01 08:00:322016-05-26 23:14:39Beyond Tax-Savings: The Benefits of an Estate Bond for your Estate Beneficiaries

https://dytucofinancialservices.com/wp-content/uploads/2016/05/Cascading-copy.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-05-01 08:00:322016-05-26 23:14:39Beyond Tax-Savings: The Benefits of an Estate Bond for your Estate Beneficiaries https://dytucofinancialservices.com/wp-content/uploads/2016/05/Questions-000103-0018-001260.jpg

1701

2400

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-05-01 06:39:502016-05-31 21:13:21Understanding your life insurance options

https://dytucofinancialservices.com/wp-content/uploads/2016/05/Questions-000103-0018-001260.jpg

1701

2400

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-05-01 06:39:502016-05-31 21:13:21Understanding your life insurance options https://dytucofinancialservices.com/wp-content/uploads/2016/04/What-are-the-tax-risks-square-image2-1.jpg

2400

2400

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-04-27 00:18:482016-04-30 23:31:40What are your risks of paying higher taxes in an emergency?

https://dytucofinancialservices.com/wp-content/uploads/2016/04/What-are-the-tax-risks-square-image2-1.jpg

2400

2400

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

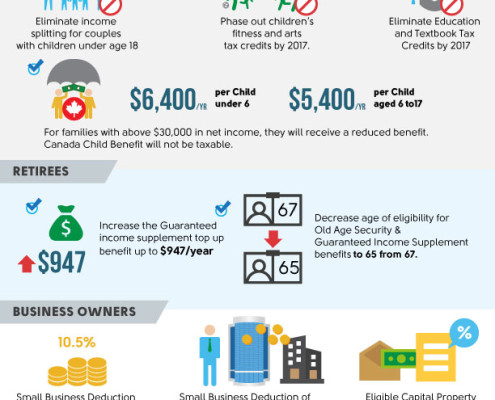

Dytuco Financial2016-04-27 00:18:482016-04-30 23:31:40What are your risks of paying higher taxes in an emergency? https://dytucofinancialservices.com/wp-content/uploads/2016/04/federalBudgetv1.jpg

792

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-04-07 11:13:392016-04-07 22:05:16Federal Budget 2016

https://dytucofinancialservices.com/wp-content/uploads/2016/04/federalBudgetv1.jpg

792

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-04-07 11:13:392016-04-07 22:05:16Federal Budget 2016 https://dytucofinancialservices.com/wp-content/uploads/2016/04/exemptTestLegislation-1.jpg

792

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-04-01 20:41:032016-08-26 15:37:38Tax-Exempt Legislation Changes

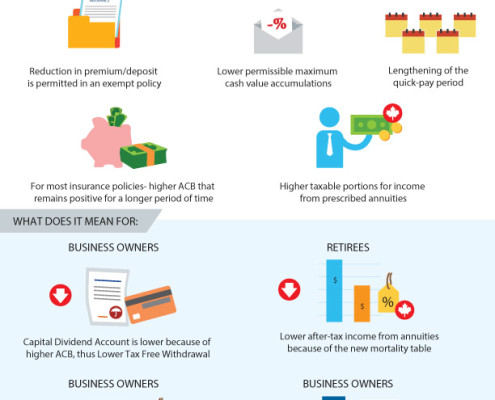

https://dytucofinancialservices.com/wp-content/uploads/2016/04/exemptTestLegislation-1.jpg

792

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-04-01 20:41:032016-08-26 15:37:38Tax-Exempt Legislation Changes https://dytucofinancialservices.com/wp-content/uploads/2016/01/Estate-Bond.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-04-01 08:00:572016-11-04 18:08:48A Lifetime Gift for Your Grandchildren

https://dytucofinancialservices.com/wp-content/uploads/2016/01/Estate-Bond.jpg

200

600

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-04-01 08:00:572016-11-04 18:08:48A Lifetime Gift for Your Grandchildren https://dytucofinancialservices.com/wp-content/uploads/2016/03/budget-1.jpg

688

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

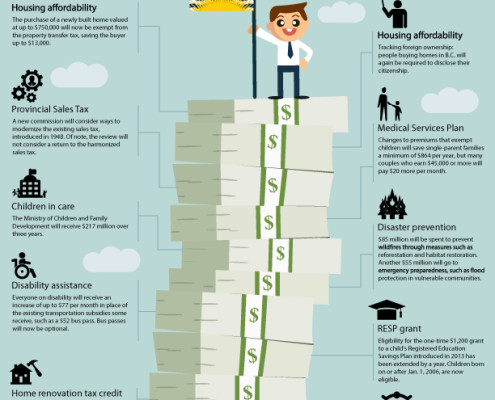

Dytuco Financial2016-03-19 20:25:432016-04-07 21:35:13BC Budget Changes

https://dytucofinancialservices.com/wp-content/uploads/2016/03/budget-1.jpg

688

612

Dytuco Financial

https://dytucofinancialservices.com/wp-content/uploads/2016/10/Header-image-Medy-Different-Perspective-smaller.jpg

Dytuco Financial2016-03-19 20:25:432016-04-07 21:35:13BC Budget Changes